Few industries carry as much risk on their shoulders as financial services. Banks, lenders, brokers, accountants, superannuation funds and fintech firms all hold two things criminals badly want: money, and the personal information that can be used to steal more of it. That combination makes cyber security for financial services a board-level concern rather than a back-office afterthought.

For Australian firms, the pressure is only growing. Attacks are becoming more frequent and more costly, regulators are raising the bar, and customers expect their money and data to be safe by default. The good news is that strong security is achievable with the right priorities and a steady, ongoing approach.

This guide walks through the threats Australian financial firms face, the rules you need to meet, and the practical steps that build genuine resilience.

Why cyber security for financial services demands a different approach

Every business needs to protect itself online, but financial firms operate under a heavier set of expectations. The value of what you hold makes you a deliberate target, not just a victim of opportunity. Attackers study how money moves through your systems and look for the weakest point between a customer’s intent and a completed transaction.

There is also a trust dimension that other sectors do not feel as sharply. A retailer that suffers a breach may lose some sales; a financial firm that loses client funds or leaks sensitive records can lose its reputation, its licence, and its clients in a single stroke. Confidence is the product you are really selling, and security is what protects it.

On top of that, the regulatory environment is stricter and more specific. Where many businesses face general privacy obligations, financial firms must also satisfy prudential standards, operational resilience requirements and director-level accountability. Treating cyber security as a core part of how the business runs, rather than a cost to minimise, is what separates firms that cope well from those that scramble.

The cyber threats facing Australian financial services

The scale of the problem is easy to underestimate until you see the numbers. According to the Australian Signals Directorate’s most recent annual cyber threat report, businesses now report an average self-reported cost of around $80,850 for each cybercrime incident, a sharp rise on the year before. The same report describes a cybercrime being reported roughly once every six minutes across the country.

For financial firms, a handful of threats account for most of the damage. Business email compromise and phishing remain among the most expensive, with attackers impersonating staff, suppliers or executives to redirect payments or harvest login details. The ASD found that compromised or stolen credentials were involved in a large share of the most serious incidents it responded to, which is why protecting identities matters so much.

Ransomware is the threat that keeps directors awake. A successful attack can freeze trading systems, customer portals and payment processing all at once, and the disruption often costs more than any ransom demand. Account takeover, where criminals gain access to a legitimate customer or staff account, is another fast-growing problem, as is the risk that arrives through a trusted third party such as a software vendor or outsourced provider. Insider mistakes and deliberate misuse round out the picture, alongside denial-of-service attacks designed to knock services offline at the worst possible moment.

The pattern across all of these is that attackers rarely break down the front door. They walk in through a reused password, a convincing email, or an unpatched system that nobody got around to updating.

The regulatory environment: APRA, the Privacy Act and beyond

Australian financial firms sit inside one of the more demanding compliance landscapes in the world, and it has tightened considerably in the past two years. Understanding what applies to you is the first step toward meeting it without panic.

For APRA-regulated entities, CPS 234 has set the baseline for information security since 2019. It requires you to maintain security capabilities matched to the threats you face, define clear roles and responsibilities, test your controls regularly, and notify APRA of material incidents within 72 hours. More recently, CPS 230 came into force in July 2025 and lifts the focus to operational resilience as a whole. It asks firms to identify their critical operations, set tolerances for disruption, prove their business continuity plans hold up under severe but plausible scenarios, and manage the risk that sits with their service providers.

Beyond the prudential standards, the Privacy Act and its Notifiable Data Breaches scheme apply to most firms handling personal information, requiring you to protect that data and report eligible breaches to the Office of the Australian Information Commissioner and to affected customers. Recent privacy reforms have added a statutory right for individuals to take action over serious invasions of privacy, along with an explicit expectation that you put reasonable technical and organisational measures in place. The Cyber Security Act has also introduced mandatory reporting of ransomware payments for larger organisations, and ASIC continues to treat cyber resilience as a duty that boards and directors are personally accountable for.

| Requirement | Who it applies to | What it means for you |

|---|---|---|

| APRA CPS 234 | APRA-regulated banks, insurers and super funds | Maintain information-security capability, test controls, and report material incidents within 72 hours. |

| APRA CPS 230 | APRA-regulated entities (from July 2025) | Manage operational risk, identify critical operations, and show your continuity and supplier arrangements withstand stress. |

| Privacy Act & Notifiable Data Breaches | Most firms handling personal information | Protect personal data and report eligible breaches to the OAIC and affected customers. |

| Cyber Security Act 2024 | Organisations with turnover above $3 million | Report ransomware payments to the government within the required timeframe. |

| ASIC expectations | Directors and boards | Treat cyber resilience as a governance responsibility, not just an IT issue. |

It is worth remembering that the government’s Essential Eight mitigation strategies underpin much of this. Even where they are not strictly mandated, regulators and clients increasingly treat them as the practical benchmark for a credible security posture.

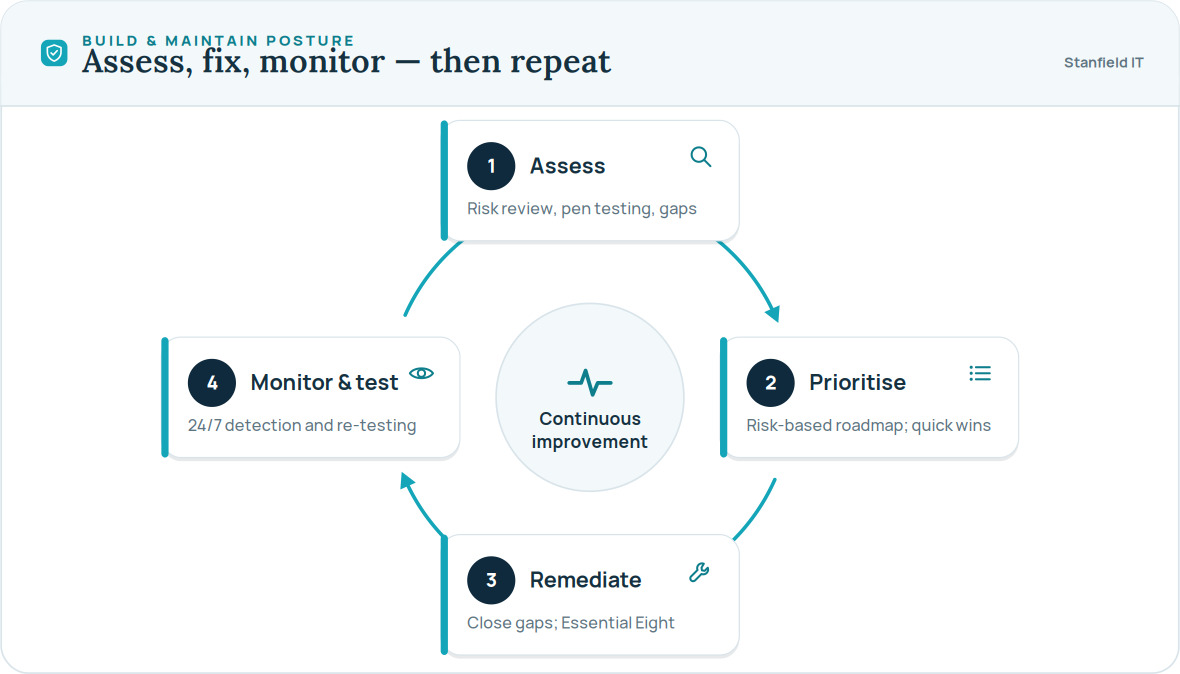

How to assess your cyber security posture

You cannot protect what you have not measured. Before investing in new tools, the most useful step is an honest assessment of where your firm stands today. This means looking at your systems, your people and your processes together, because a weakness in any one of them can undo the others.

A good assessment follows a simple, repeating cycle rather than a one-off audit that gathers dust. You work out where the real risks are, decide what to fix first, close those gaps, and then keep watching so new problems are caught early.

In practice, the assessment phase often combines a structured risk review with technical testing such as a penetration test, which safely simulates how a real attacker would try to get in. The findings let you build a risk-based roadmap, tackling the changes that reduce the most risk for the least disruption first. A formal cyber security risk assessment is the cleanest way to get this picture, especially when you also need evidence for APRA, auditors or insurers. The point is to move from a vague sense that you are “probably fine” to a clear, documented understanding of your exposure.

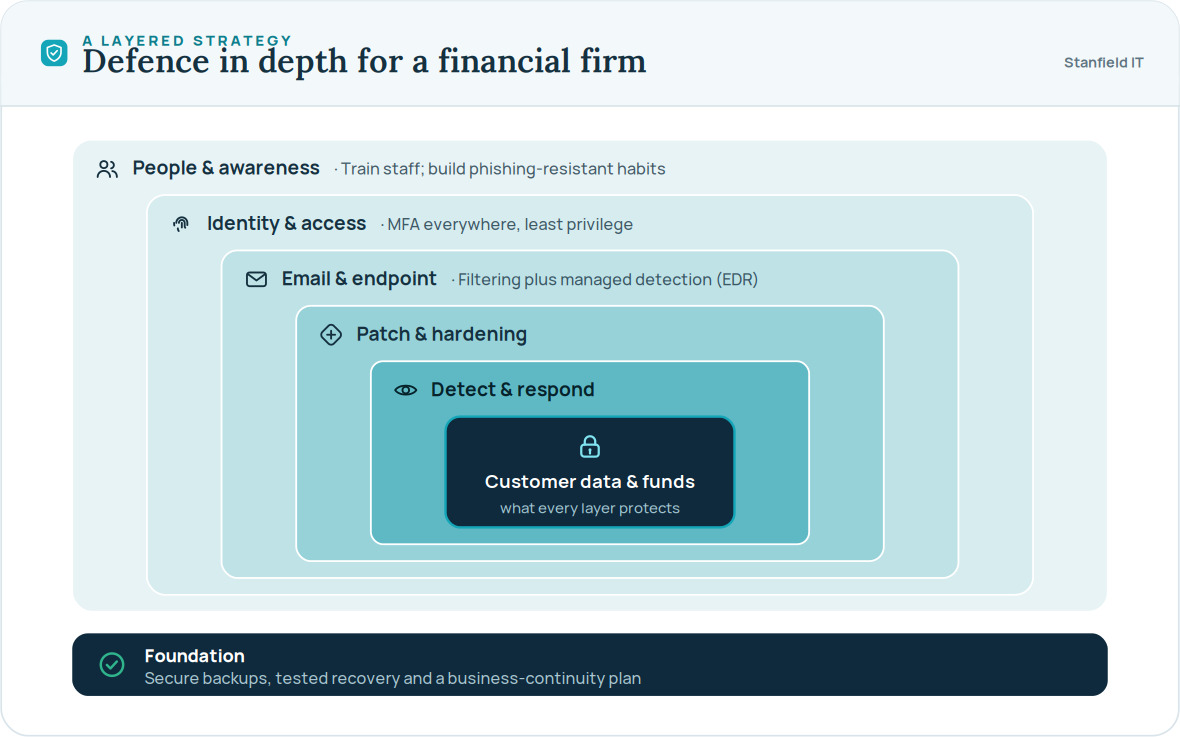

Building a layered cyber security strategy for financial services

No single control will keep a determined attacker out. Effective cyber security for financial services relies on defence in depth, where multiple layers each catch what the others miss. If one safeguard fails, the next one is there to limit the damage.

The outermost layer is your people. Staff who can recognise a suspicious email or payment request stop a large share of attacks before they begin, which is why ongoing security awareness training is one of the highest-value investments a firm can make. Inside that sits identity and access control: multi-factor authentication on every account, and the principle of giving people only the access they genuinely need.

From there, the layers become more technical. Email filtering and modern endpoint protection guard the channels attackers use most. Keeping systems patched and hardened, in line with the Essential Eight, closes the gaps that ransomware exploits. Behind all of that, continuous monitoring through a managed detection and response service watches for the early signs of an intrusion around the clock, because the difference between a contained incident and a disaster is usually how quickly it is spotted.

Underpinning every layer is the ability to recover. Secure, tested backups and a current business continuity plan mean that even a worst-case event becomes something you bounce back from rather than something that ends the business.

Common mistakes financial firms make

Most security failures are not caused by exotic, never-before-seen attacks. They come from a handful of avoidable habits that quietly leave the door ajar. The most common ones we see include:

- Treating cyber security as a one-off project instead of an ongoing discipline that needs regular attention.

- Assuming that ticking a compliance box is the same thing as being secure.

- Leaving multi-factor authentication switched off on “just a few” convenient accounts.

- Overlooking the risk that sits with third-party suppliers, software and outsourced services.

- Relying on backups that have never actually been tested with a full restore.

Each of these is straightforward to fix once it is recognised, and addressing them costs far less than recovering from the breach they eventually allow. The firms that stay safe are usually not the ones with the biggest budgets, but the ones that take care of the basics consistently.

How Stanfield IT supports cyber security for financial services

Getting all of this right while running a busy practice is a genuine challenge, and it is rarely realistic to manage every layer in-house. This is where a specialist partner in cyber security for financial services makes the difference. Stanfield IT works with Australian financial firms to design, build and maintain security that stands up to both attackers and auditors.

Our approach starts with understanding your specific risks and obligations, then putting practical controls in place across all the layers described above. That can mean round-the-clock threat monitoring and response, regular testing of your defences, help meeting APRA, Privacy Act and Essential Eight requirements, and clear plans for the day something goes wrong. If you need to demonstrate your readiness to regulators or clients, our cyber security services provide both the protection and the evidence.

Just as importantly, we explain things in plain language. You should never feel locked out of decisions about your own firm’s security, and a good provider helps you understand the trade-offs rather than hiding behind jargon.

Building resilience for the long term

Cyber security for financial services is not a problem you solve once and forget. The threats keep evolving, the regulations keep tightening, and your own systems keep changing as the business grows. What protects you is a proactive, layered approach backed by regular assessment and the ability to recover quickly when tested.

The firms that thrive treat security as part of how they earn and keep trust, not as a reluctant expense. Get the fundamentals right, stay alert to new risks, and make sure someone is always watching, and you turn cyber security from a source of anxiety into a genuine competitive strength.

If your firm wants reliable, proactive protection that satisfies both attackers’ tests and regulators’ expectations, Stanfield IT can help. Talk to our team on 1300 910 333 or get in touch for a straightforward conversation about where your business stands today.